The Future of Carbon Markets

As London prepares to host the Carbon Unbound Summit, attention is laser-focused on carbon removal and the race to extract CO₂ from the atmosphere and lock it away for centuries. While reducing emissions is non-negotiable, a new wave of investment is flowing into projects that actively remove carbon, shifting climate action from theory into measured tonnes of carbon delivered. But where is the money really going? Who are the solution providers leading the charge, and how effective is this market so far, both in promises (purchases) and in practical results (deliveries)?

Market Dominance and Buyer Concentration

The CDR market remains heavily concentrated among technology giants, with Microsoft accounting for 91% of all long-term removal agreements in the first half of 2025. This staggering concentration reflects both the enormous capital requirements and the strategic importance these companies place on carbon neutrality. Google has also emerged as a major player, tripling its CDR investment to over $100 million in 2024 (Roberts , 2025), demonstrating how AI-driven emissions increases are forcing tech companies to invest heavily in removal technologies.

The buyer concentration presents both opportunities and risks. While these major purchasers provide essential market-making functions, the sector desperately needs broader participation to achieve sustainable growth. Currently, 50% of buyers in the first half of 2025 were first-time participants, contributing approximately 6 million credits and representing positive momentum toward market diversification (Balaji, 2025).

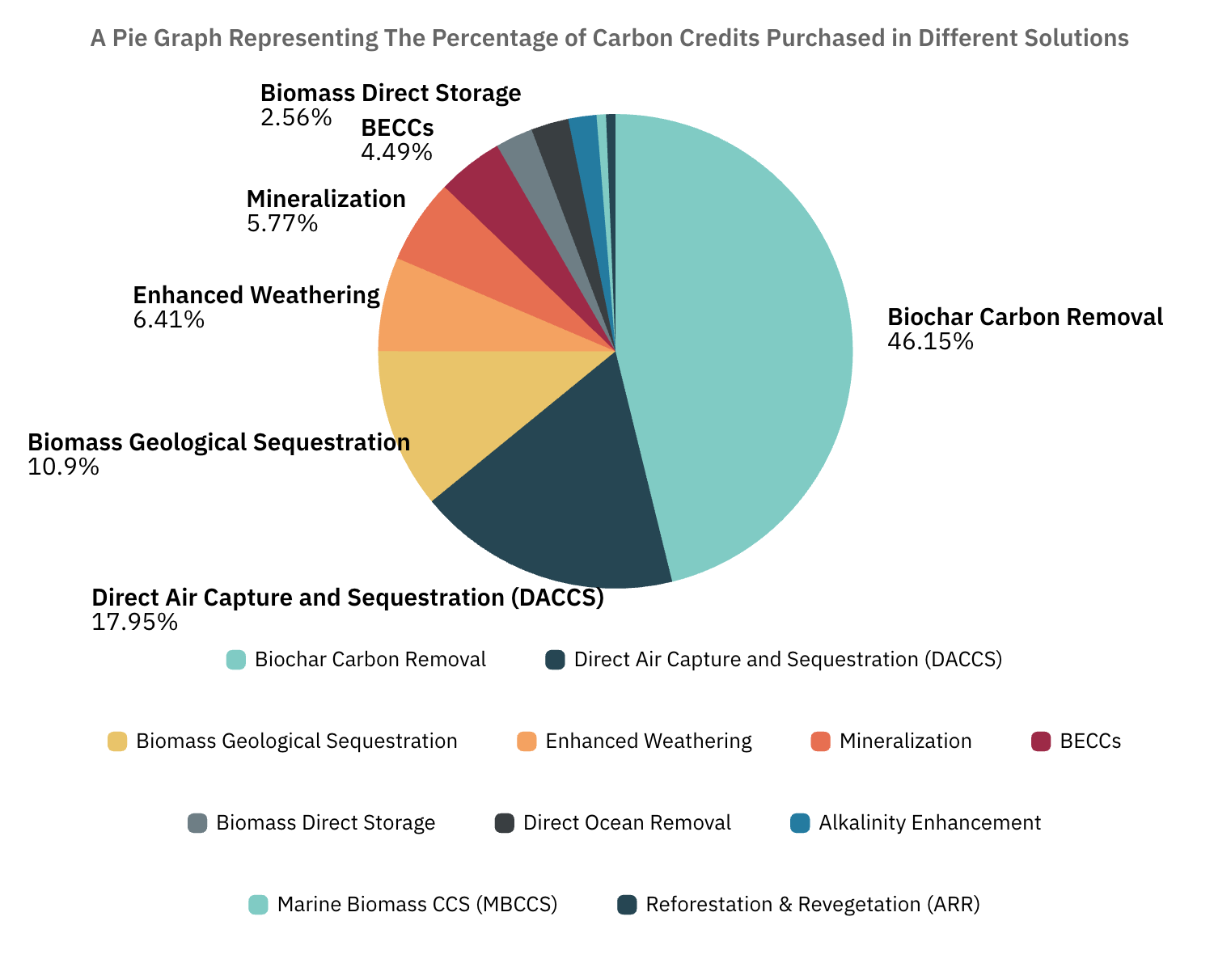

Biochar Carbon Removal: The Undisputed Market Leader

Biochar carbon removal dominates the CDR landscape, capturing 46% of the total market by purchase volume. This ancient technique, refined with modern science, transforms agricultural and forestry waste into stable carbon through pyrolysis. A process that prevents organic matter from decomposing and releasing CO₂ back into the atmosphere.

The technology's appeal extends beyond pure carbon removal. Biochar projects deliver measurable co-benefits including improved soil fertility, increased water retention, and reduced need for chemical fertilizers. These additional advantages make biochar particularly attractive to buyers seeking comprehensive environmental impact rather than just carbon accounting.

Leading Biochar Suppliers

- Exomad Green (Bolivia)

Exomad Green stands as the undisputed leader with over 1.7 million tonnes contracted. The company operates as the world's largest biochar producer, removing 120,000 tonnes of CO₂ annually across two facilities while delivering significant co-benefits to over 250,000 people in local communities. Their unique model converts sustainably sourced forestry residues into biochar distributed to local farmers, improving both soil health and agricultural productivity.

- Charm Industrial (USA)

Charm Industrial (USA) has pioneered dual-product biochar operations, contracting over 112,000 tonnes through innovative mobile pyrolyzers that operate directly on farms. Beyond biochar, Charm produces bio-oil for permanent geological storage, maximizing carbon removal from each tonne of biomass processed.

- Varaha (India)

Varaha (India) secured a major 100,000-tonne agreement with Google, positioning India as a competitive global hub for biochar production due to favorable production costs and abundant biomass feedstock.

Supply constraints are emerging rapidly across the biochar sector. Recent analysis shows 62% of high-quality biochar capacity for 2025 is already locked into offtake agreements, with 28% secured through 2026. Companies relying on spot market purchases face 18% price increases and shrinking availability, forcing strategic buyers toward long-term offtake agreements (You, 2025).

BECCS: The Industrial-Scale Solution

Bioenergy with Carbon Capture and Storage (BECCS) has emerged as the method of choice for mega-scale deals, accounting for 89.6% of the six largest contracts by volume in Q2 2025. BECCS involves capturing CO₂ from the flue gas of industrial biogenic processes, typically ethanol production or biomass combustion, then storing it permanently underground. (CDR.fyi, 2025)

Microsoft's largest-ever CDR purchase exemplifies BECCS's potential: a $800 million deal with AtmosClear for approximately 7 million tonnes, representing the largest carbon removal contract in history. The appeal of BECCS lies in its ability to leverage existing industrial infrastructure while delivering higher CO₂ concentrations that make capture less expensive than direct air capture.

BECCS projects can retrofit existing pulp and paper plants or heat and power facilities with CO₂ capture units, offering one of the easiest pathways to removing hundreds of thousands of tonnes per year. This industrial integration makes BECCS particularly attractive for buyers seeking immediate scale rather than waiting for greenfield projects to mature (CDR.fyi, 2025).

Direct Air Capture: The High-Tech Frontier

Direct Air Capture with Carbon Storage (DACCS) represents 18% of the market but captures disproportionate attention as the technological frontier of carbon removal. DACCS plants use chemical processes to extract CO₂ directly from ambient air and store it permanently underground, offering unparalleled permanence and scalability potential.

Leading DACCS Projects and Suppliers

- Climeworks

Climeworks (Switzerland/Iceland) operates the world's largest DAC facilities, including the 36,000-tonne capacity Mammoth plant in Iceland. Powered by abundant geothermal energy, Climeworks has delivered more verified removals than any other DAC company, though they face ongoing technical challenges with filter durability that have prevented them from reaching full nameplate capacity.

- 1PointFive (USA)

1PointFive (USA) is preparing to launch the Stratos facility in Texas with 500,000 tonnes annual capacity by end-2025. This represents a significant scale-up from existing DAC operations and includes partnerships with major buyers including JP Morgan and Palo Alto Networks. Occidental is also developing a second facility in South Texas with backing from ADNOC's XRG investment arm and a $650 million U.S. Department of Energy grant.

Despite enormous promise, DAC faces significant challenges. Costs remain high at $300+ per tonne, and projects require massive amounts of clean electricity—creating competition with AI data centers and other renewable energy demands. The 45Q tax credit in the U.S. provides $180 per tonne for DAC projects, but long-term policy support remains uncertain.

Biomass Carbon Removal and Storage: The Hybrid Approach

Biomass Carbon Removal and Storage (BiCRS) methods, including bio-oil injection and direct biomass burial, represent 10.9% of credits purchased. These approaches combine the abundance of natural biomass with the permanence of geological storage, offering a rapidly scaling middle ground between nature-based and engineered solutions.

Charm Industrial has pioneered bio-oil injection beyond their biochar operations, converting agricultural residues into carbon-rich liquid pumped into EPA-regulated underground wells. Their approach has permanently removed over 6,200 tonnes to date—more direct removal than any other permanent CDR supplier.

Vaulted Deep (USA) emerged as the breakout BiCRS company of 2024, taking organic waste including biosolids, manure, and agricultural residues and injecting them directly underground. The company raised $32 million in Series A funding and has already delivered over 18,000 tonnes of CDR while diverting 69,000 tonnes of waste from surface disposal. Their $58.3 million offtake agreement with Frontier buyers represents the largest BiCRS deal to date.

Market Dynamics: The Purchase vs. Delivery Gap

One of the most striking aspects of the CDR market is the massive gap between purchases and deliveries. While companies have contracted over 61.5 million tonnes in the first half of 2025 alone (Roberts , 2025), only a small fraction has been actually delivered and verified. This reflects the industry's nascent stage, where forward contracts are essential to provide suppliers with the certainty needed to invest in scaling production.

Biochar leads in delivery rates, accounting for 89.4% of the total 116.8 thousand tonnes delivered in Q2 2025 (CDR.fyi, 2025), with BiCRS methods accounting for another 6.6%. Meanwhile, DACCS faces the classic "order more than you can ship" dilemma, with only a small fraction of contracted credits delivered as plants require significant time, capital, and regulatory approval.

Pricing Trends and Market Evolution

The CDR market is experiencing rapid price evolution as technologies mature and competition increases. Average prices decreased from $490 per tonne in 2023 to $320 per tonne in 2024, though significant variation exists across methods. Biochar ranges from $100-$200 per tonne but shows 18% price increases due to supply constraints, while DACCS remains at $300+ per tonne (CDR.fyi, 2024).

However, a significant pricing gap exists between buyer willingness to pay and supplier profitability requirements. Suppliers indicate breakeven prices of $140-$340 per tonne for 2030 delivery, with reasonable profit margins requiring $180-$430 per tonne. This gap must close for sustainable market growth.

Looking Forward: The Catalytic Moment Attending Carbon Unbound, London: October 21–22, 2025

Event Details:

- Dates: 21–22 October 2025

- Location: 155 Bishopsgate, London, UK

- Who’s Going: 400+ C-level founders, investors, policy shapers, and market experts.

- What to Expect: Mainstage presentations, tactical panels, small-group campfire sessions, start-up pitches, buyer–supplier matchmaking, and peer-to-peer networking—plus an attendee app for planning meetings and maximizing connections

The Bottom Line: Carbon Removal Can’t Wait

Carbon Unbound Europe sets the agenda for Europe’s carbon removal journey, with a program laser-focused on:

- Accelerating CDR with AI and technology breakthroughs

- Advancing investment trends, new financing models, and robust regulatory frameworks

- Elevating the integrity of the carbon market—CDR credit quality, MRV standards, and scaling supply to meet global demand

- Highlighting the role of the Global South, cross-sector partnerships, and integrating nature-based and tech-driven solutions

- Direct, actionable sessions dedicated to outcomes and real-world impact

Join the Carbon Unbound Europe Summit in London this September.

For the latest on carbon removal solutions, market trends, and the complete summit agenda, visit Carbon Unbound Europe and become part of the movement shaping climate leadership and gigaton-scale removal.

https://www.carbonunboundeurope.com/

Acknowledgements

Thank you for exploring How the World’s Fastest-Growing Carbon Removal Markets Are Shaping Our Climate Future We would like to further thank CDR.fyi for their data creation published within this article.

Roberts , L., 2025. CDR offtakes reach 61.5 mln tCO2e in H1; tech giants continue to drive demand, s.l.: Fast Markets.

Balaji, P., 2025. State of the Market: CDR (2025), s.l.: Allied Offsets.

You, M., 2025. The new renewable revolution: Why carbon dioxide removal will transform the carbon market, s.l.: World Economic Forum.

CDR.fyi, 2025. 2025 Q2 Durable CDR Market Update - Biggest Quarter Ever, s.l.: CDR.fyi.

CDR.fyi, 2025. 2025 Q1 Durable CDR Market Update - Back at Basecamp , s.l.: CDR.fyi.

CDR.fyi, 2024. 2024+ Market Outlook Summary Report, s.l.: CDR.fyi.

.png)